Debt increases are particularly striking in advanced economies, where public debt rose from around 70 per cent of GDP in 2007 to 124 per cent of GDP in 2020….reports Asian Lite News

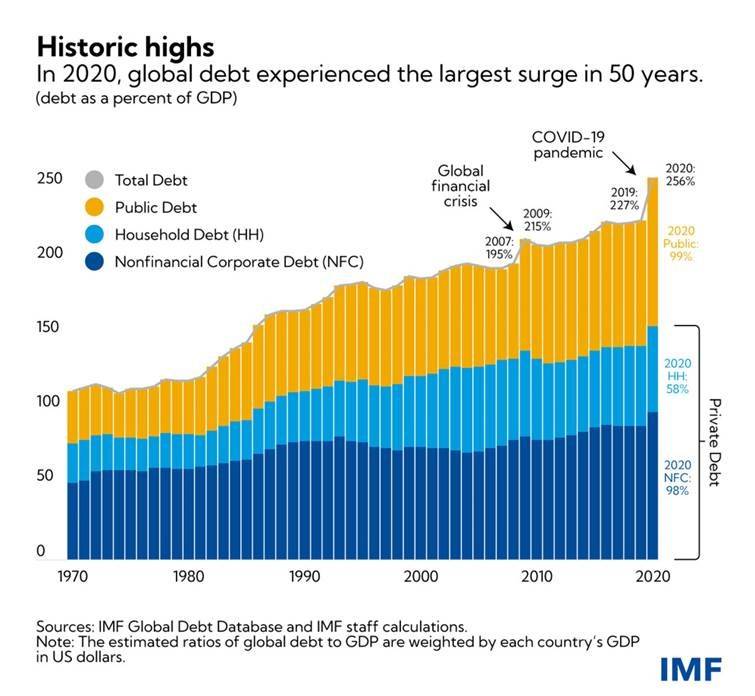

Global debt rose to a record $226 trillion in 2020 as the world was hit by the raging Covid-19 pandemic and a deep recession, the International Monetary Fund (IMF) announced.

Global debt rose by 28 percentage points to 256 per cent of gross domestic product (GDP) in 2020, the largest one-year debt surge since World War II, Vitor Gaspar, director of the IMF’s Fiscal Affairs Department, wrote in a blog on Wednesday with his colleagues, citing figures from the IMF’s latest Global Debt Database.

Debt increases are particularly striking in advanced economies, where public debt rose from around 70 per cent of GDP in 2007 to 124 per cent of GDP in 2020.

Meanwhile, private debt rose at a more moderate pace from 164 to 178 per cent of GDP in the same period, according to the IMF.

ALSO READ: Chinese debt trap: Lanka going Ugandan way

The IMF officials noted that a crucial challenge for policymakers is to “strike the right mix of fiscal and monetary policies in an environment of high debt and rising inflation”, as the debt surge amplifies vulnerabilities.

“The risks will be magnified if global interest rates rise faster than expected and growth falters. A significant tightening of financial conditions would heighten the pressure on the most highly indebted governments, households, and firms,” they said.

The IMF officials suggested that some countries, especially those with high gross financing needs or exposure to exchange rate volatility, may need to adjust faster to preserve market confidence and prevent more disruptive fiscal distress.

In addition, the pandemic and the global financing divide demand strong, effective international cooperation and support to developing countries, they noted.